Introduction

Coronavirus has affected our way of living and doing business and life isn’t the way it used to be before.

SMEs are struggling to keep afloat, and so many if not thousands have lost their jobs and those who are still employed are very fortunate. Whilst the opportunity is now with the employed, it is now high time to think seriously on how best you can save some money preparing for pandemics like Covid-19, Natural Disasters and other related disasters and unforseen needs that may arise or better still for early retirement.

In Papua New Guinea most of the employed are so lazy thinking that putting some money through government sanctioned channels like superannuation contributions, and or savings and loan societies is enough. When you resign, or lose your job or retire, you will find that you haven’t saved enough and cannot do much about it.

I have worked in the superannuation industry for eight(8) years, and savings and loan societies for four(4) years and have seen how reckless our working class are. Even me included. I could just apply for loan to just drink beer which led to my going into a lot of bad debts, both with loan sharks and peer to peer lending or dinau moni. I’ve never thought of saving those extra money’s for the bad days ahead. I was all reckless in saving.

Whilst like many others, I learnt my lesson the hard way. In this blog I will be discussing my thoughts three ways I think are the best and effective ways on how you could save some money using existing and proven methods.

Without further ado, let’s go straight there.

1. Voluntary Contributions With Superannuation funds.

Voluntary Contributions to Superannuation funds is a very effective way to boost your savings. In fact our superannuation funds in Papua New Guinea encourage voluntary contributions.

How is voluntary contributions done?

Every fortnight from your pay, your employer deduct’s 6% of your salary to the nominated superannuation fund. Your employer contributes 8.4% on your behalf bringing to a total of 14.4% going to superannuation.

You have a option to increase your portion up to 15%. In this way, you increase your chances of saving quickly to reach your target and retire early whilst you are still young and enjoy your hard earned cash.

You can visit the nearest super fund branch and enquire for more information or collect the application form to fill and start saving.

Whilst still on superannuation, you can also do salary sacrifice to save even more and save fast for early retirement. Remember, time is our enemy therefore, doing everything and anything using proven methods to retire early should be our aim.

So what is SALARY SACRIFICE and how do I do that?

Super funds also allow this option. To do a salary sacrifice, you can arrange with your payroll to have portion of your salary (annual gross) sacrificed to be added on your employer’s portion so it goes in before tax. This is another way to reduce tax on your salary. Visit your super fund branch for more information on this option.

Notable supera funds that provide the avenues discussed above are Nasfund and Nambawan Super Limited .

2. Savings and Loan Societies.

Savings and Loan Society is another best option to increase your chances of saving more for early retirement. All savings and loan societies in Papua New Guinea have a minimum requirement of K20 to start saving but unlike super funds, you are allowed to do cash deposits as well.

The disadvantage of savings and loan societies is that you are allowed to withdraw your savings so long as it has a minimum of K200 in the savings account.

However, following are the advantages of savings and loan societies:

- You can do cash contributions/deposits

- Withdraw anytime when you need cash for emergency situations

- You can deposit any amount to boost your savings

- More than 10% including special savings accounts such as “school fees club’s account” and “Christmas Club account”.

Call in to the nearest savings and loan society office and enquire for more.

Further, the interesting thing about savings and loan society that I like is the number of special accounts with their interest rates. The interest for general purpose/savings account is 2% annually, whereas all other special purpose accounts are 6% annually when added together, you have a total of 14% annually. This is just awesome. You will definitely make a fortune for yourself utilizing the savings and loan products provided you control your borrowing habits with the society(savings and loan).

If you have extra cash, you can do peer to peer lending to increase your capital thus increasing the amount to deposit cash to your savings and loan account to attract the 14% interest discussed above.

There are number of savings and loan societies in the country but the most notable ones that I can recommend you to check are Teachers Savings and Loan Society Limited, Nambawan Savings and Loans Society Limited, Nasfund Contributors Savings and Loan Society Limited, etc.

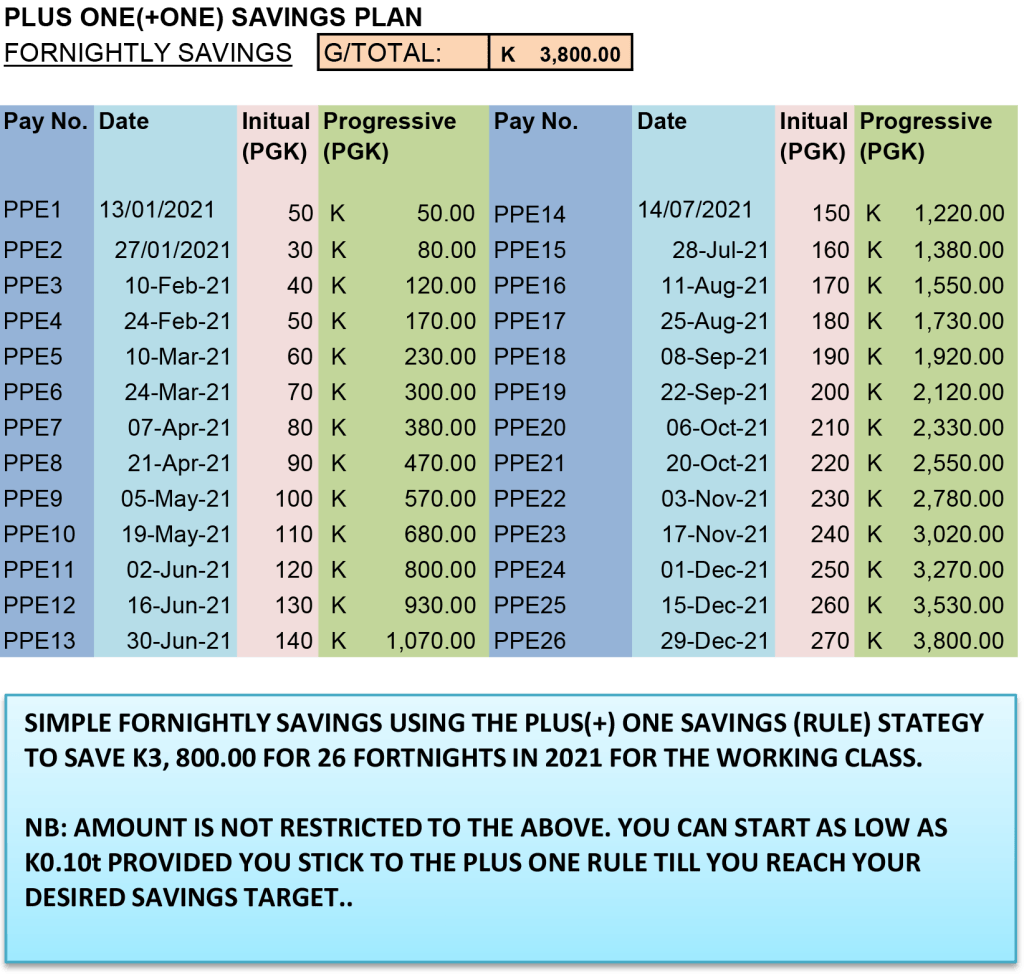

3. Fortnightly Savings to Secondary Account using the Plus One(+1) Savings Method.

Plus one savings method is my personal favorite. In fact you can teach this method to your kids so they can start with K0.10 and learn the art of savings at a early age to secure their own financial goals.

Plus One Savings Method is a method in which you add one part of the principal amount ontop of the previous amount contributed, each amount, each given day in your own convenience. Study the method (example) given/insert photo above to see how it’s done.

I have enquired at Bank South Pacific and was told that you can have a secondary account with the bank.

Given that opportunity, you can open a secondary account with BSP and transfer your contributions via SMS banking or internet banking every fortnight for 26 fortnights and see how much you have saved.

The key to savings or building wealth requires commitment, determination, hardwork, and ALOT of patience.

This strategy is very effective. There’s a separate blog post on this subject giving details on how you can use this method on this link.

For the benefit of this blog post, I’ll discuss little bit on this method.

First, you must have a steady flow of income, which you already have, your fortnight pay.

Secondly, open a secondary account with the bank where you receive your salary from.

Third, start saving by transferring your prescribed portion to your secondary account.

Lastly but not the least, thank me after you see your savings grow. Hahaha, just kidding there, but that is the way to effectively save during this very difficult economic times we are in.

This method will take a lot less time than you think, and you can do it in very small amounts each fortnight.

Here’s an extract from my previous blog on this method.

100Days Savings with the Plus One method.

For instance, let’s say, we start savings with K1.00 on day one, and K100 on the 100th day.

If we were to start with K1, this is how it will be. Since its 100 days, a day is equivalent to the amount we drop in the penny box or save for that matter.

On day 1, we save K1,

On day 2, we save K2, giving as a total of K3,

On day three, we save K3, giving us a total of K6 and so on until we reach day number 100, we save K100, giving us a total of K5, 050. Boom! You made yourself a lot of money. No tax, no bank fees, no bank queues, but just your penny box and your disciplined action with commitment to invest in yourself.

This is the method that can be used for fortnightly contributions.

NOTE: Amount is not restricted plus number of contributions is noted restricted as well.

Conclusion

The key to building wealth is developing good habits—like regularly putting money as little as K0.10 away every day. If you make investing a habit now, you’ll be in a much stronger financial position down the road.

All it requires from your part is, planning, set target, commitment and discipline. That’s all you need, to go down the journey to financial freedom. You don’t have to rely on your superannuation contribution and finish pay from your employer as the only means available to cash out at retirement.

There are so many different ways you can utilize whilst working to increase your savings. And like the common phrase, don’t put your eggs in the same basket is true in this sense.

Disclaimer

Whilst the author has used his best efforts in this blog, he makes no warranty or representation of the organization’s mentioned herein, nor any representation with respect to the accuracy of the content of this blog and specifically disclaim any implied warranties of merchantability or finances for a particular purpose.

It is further acknowledged that no warranty of any kind may be created or extended by any written sales materials or sales representatives.

The information contained in this guide is for information purposes only and may not apply to your situation. It is advisable that you consult a financial expert or legal professional where appropriate before using this guide and users of this material assume risk.

The author shall not be liable for any loss of profit or salary or any other damages resulting from use of this guide. All links are for information purposes only and are not warranted for.content, accuracy or any other implied or explicit purpose.

Please keep this in mind when reviewing this guide.